Editorial & Legal Accuracy Notice (Louisiana)

This blog contains general legal and safety information and is not legal advice. Laws and deadlines can change, and outcomes depend on specific facts.

Last reviewed / updated: March, 2026

Reviewed, updated, and authored by: Stephen Babcock, Louisiana injury lawyer

This guide explains who may be legally responsible after a Louisiana food delivery accident and what evidence helps identify the right insurance coverage.

When a DoorDash or Uber Eats driver crashes in Louisiana, the question is not just fault—it is which policies and companies are actually in play. We are not built for volume. We are built for leverage. Speed + evidence preservation + insurer-insider knowledge + trial-ready preparation = The Babcock Benefit. In a food delivery accident, leverage often comes from proving app status, preserving video, and matching the claim to the right coverage.

Food delivery wrecks can feel simple at the scene and complicated a week later. The reason is that a delivery case can involve multiple policies, multiple vehicles, and multiple “who was responsible” narratives. This post gives you a practical way to identify who to pursue and what to document so the story cannot be rewritten after the fact.

If you are inside the first 72 hours, call (225) 500-5000 or use the free case review form before evidence changes.

Firm links: Client Reviews | Contact | Locations

Prefer a print-friendly checklist and both infographics in one place? Download the printable toolkit (PDF) and keep it with your claim notes.

Who Can You Sue After a Food Delivery Accident in Louisiana?

In most Louisiana food delivery accident cases, you start with the at-fault driver and any other driver who contributed to the crash. Because Louisiana Civil Code article 2315 centers liability on fault that causes damage, the facts about vehicle ownership, job control, and coverage can expand the list of defendants.

- The delivery driver (and the driver’s insurer)

- Another at-fault driver (and that driver’s insurer)

- The vehicle owner if different from the driver

- An employer or contractor entity when the driver was working

- A delivery platform entity in limited, fact-specific situations

- A business or property owner only when its own negligence contributed

Start with the people and entities tied directly to the vehicles and the driving decisions. Then work outward to who owned the car, who controlled the work, and whose insurance should respond. If you want a practical overview of the investigation sequence, see how we build delivery-driver claims.

Driver Fault and Negligence

Most cases still turn on ordinary driving mistakes like unsafe lane changes, following too closely, or distracted driving. In Louisiana, Civil Code article 2316 recognizes responsibility for negligence, which is why photos, witness accounts, and a clear timeline matter from day one.

Vehicle Owner and Permission

If the delivery driver was using someone else’s vehicle, the owner may matter in the coverage analysis even when the owner was not driving. Ownership and permissive-use details can affect which policy is primary, which is one reason we ask for the vehicle registration early instead of guessing later.

Employer Responsibility and Course-and-Scope Issues

When a delivery driver is an employee acting in the course and scope of work, Louisiana Civil Code article 2320 is a core source people look to for employer responsibility. The hard part is that many delivery arrangements are structured to argue “not an employee,” so you often have to prove the practical facts about control, dispatch, and expectations.

Other Defendants Beyond Driving

Sometimes the “who can I sue” question is really about a second cause of the crash, like a defective part or a dangerous product that failed. When a product defect is truly in play, Louisiana’s Product Liability Act can control how those claims must be framed.

Does DoorDash, Uber Eats, or Other Delivery App Insurance Cover the Crash?

Sometimes, but the answer usually depends on the driver’s app status at the time of the wreck and the policy wording. Uber’s insurance overview explains that coverage can change depending on whether a driver is offline, online waiting, or on an active trip or delivery.

| Driver Status (Example) | What to Document Right Away |

|---|---|

| App off or logged out | Driver identity, vehicle ownership, personal policy details, and any other at-fault parties |

| Logged in and waiting | Screenshots showing status, time stamps, and whether a request was pending |

| Accepted an order and en route | Order ID, pickup/drop-off details, in-app navigation data, and dispatch communications |

| Active delivery in progress | Delivery timeline, GPS data if available, and confirmation screens showing the active period |

Delivery cases also create a “policy stacking” problem: the driver’s personal policy may be first, and any platform coverage may be contingent or excess depending on the period and the claim type. Uber’s coverage explainer is a useful example of why proving the driver’s exact status window is often the turning point.

DoorDash states in its Dasher insurance explanation that it provides third-party auto liability insurance for certain accidents during defined delivery periods. This is why we focus early on proving the exact minute the driver was “available,” “assigned,” or “delivering,” because insurers often fight about the period rather than the crash itself.

Can You Sue the Delivery App Company?

Sometimes, but it is usually fact-driven and heavily contested, especially when the company argues the driver is an independent contractor. Because Civil Code article 2320 is tied to employee responsibility, the classification and control facts can make or break this part of a food delivery accident case.

- Vicarious liability theory: Was the driver an employee acting within the job’s scope?

- Direct negligence theory: Did a company’s own decisions create an unreasonable risk?

- Coverage theory: Does a platform policy apply to this app-status period?

- Identity theory: Which entity actually contracted for the delivery work?

Expect this part of the case to turn on documents, not vibes: contracts, app records, dispatch prompts, and how the work was managed in practice. That is what we mean by leverage: when an insurer tries a “not our driver” story, you answer with a timestamped record and move on.

Timeline Builder: What to Do in the First 72 Hours

Your first 72 hours are about capturing facts that disappear, especially app data and video that may overwrite quickly. This is why we push to preserve app status evidence and nearby camera footage before it is lost or re-recorded.

- Lock down app proof: Screenshot the driver’s delivery screen, your order receipt, and any texts.

- Photograph the whole scene: Take wide shots, close-ups, and license plates.

- Get witnesses: Names, phone numbers, and where they were standing.

- Preserve video fast: Ask businesses to save footage and note camera locations.

- Write a same-day timeline: Time, place, traffic, weather, and what was said.

Talk to a Lawyer Quickly If Any of These Are True

Some situations create fast-moving deadlines or proof problems that are hard to fix later. If any of these apply, it is smart to talk to counsel quickly so the right preservation steps happen first.

- The delivery driver or insurer is pushing a quick recorded statement

- The vehicle is about to be repaired, towed away, or declared a total loss

- You suspect a commercial policy or platform policy might apply

- You need video from a business, apartment complex, or driveway camera

- Fault is disputed and witnesses are not cooperating

Evidence Blueprint: The Records That Win Delivery-Driver Claims

A strong delivery crash claim is usually built by connecting three things: app status, driving fault, and losses you can document. When you build those records early, it becomes harder for an insurer to shrink the claim by creating “proof gaps.”

- App status file: screenshots, order IDs, time stamps, and dispatch messages

- Crash file: photos, witnesses, body-cam info, and any dash-cam sources

- Vehicle file: registration, repair estimates, and pre-repair photos

- Loss file: bills, missed work notes, and a symptom and activity journal

- Coverage file: declarations pages, denial letters, and claim numbers

If you are evaluating whether a delivery driver crash should be treated as a commercial-type claim, it helps to compare it to other work-vehicle cases. Our commercial vehicle accident page explains the kinds of documents that often matter when work activity affects coverage and responsibility.

What we see in practice

In delivery cases, we see insurers fight hardest over app status and coverage timing, not just who ran the red light. We also see small documentation gaps get used as “reason to doubt” narratives unless the record is built early.

- Video disappears before anyone sends a preservation request

- Adjusters focus on coverage periods more than crash facts

- Drivers and platform entities point at each other to avoid responsibility

- Vehicle repairs happen before the best photos and measurements are taken

- People underestimate how much a clear timeline improves credibility

We also see that food delivery accidents are often treated like “just a car wreck” until a coverage denial shows up. Once that happens, the dispute can turn into a paperwork fight with multiple carriers. This is why we treat the app evidence and the insurance paperwork as part of the liability case from the start.

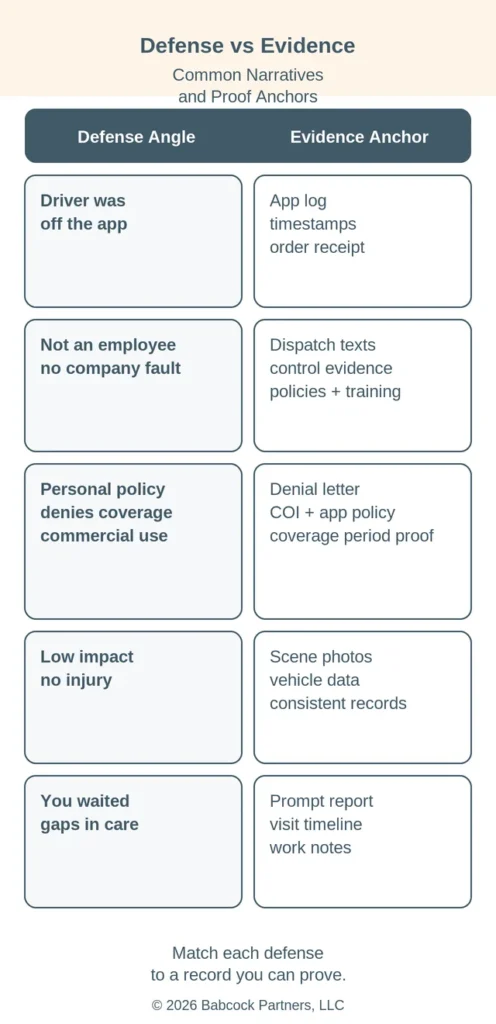

Defense Audit: What Insurers Argue and How You Prove It

Insurance defense themes in food delivery accident claims are predictable, which is helpful because you can prepare for them. The best response is a simple record trail that answers each narrative with a document, photo, or time stamp.

| Common Defense Narrative | Evidence Anchor That Helps |

|---|---|

| “The driver was not working.” | App screenshots, order receipt, and time-stamped location and dispatch data |

| “The company is not responsible.” | Contracts, training materials, and proof of how the work was controlled in practice |

| “Coverage does not apply.” | Declarations pages, denial letters, claim numbers, and proof of the app-status period |

| “Minor impact means minor injury.” | Photos, repair documentation, and consistent records of symptoms and limits |

| “You waited too long.” | Same-day notes, appointment timeline, and consistent follow-up documentation |

If you want the longer practice-area overview, our Baton Rouge delivery vehicle accident practice page explains how we investigate delivery-driver crashes and coordinate the coverage proof with the liability proof.

What Compensation Categories Are Usually in Play?

The goal of a negligence claim is to recover the losses that were actually caused by the crash, and Civil Code article 2315 is the foundational “fault causes damage” principle people often start with. This is why we track each category early so an adjuster cannot quietly minimize it later.

- Medical bills and future care needs supported by records

- Lost income and work limitations supported by pay and job documents

- Property damage and related out-of-pocket costs

- Pain, suffering, and day-to-day limitations shown by consistent documentation

Even when you have good liability proof, damages can rise or fall based on organization. A symptom-and-activity journal, work notes, and consistent appointments can make the damages story easier to understand without exaggeration.

How a Lawyer Builds the Case in a Food Delivery Accident

A delivery accident case is built by separating what happened from who pays, then proving both with records. When the investigation is done early, you can often prevent the “coverage confusion” delay that insurers use to stall and pressure settlements.

- Identify every policy: personal, commercial, and any platform policy tied to status periods.

- Preserve digital evidence: app screenshots, receipts, GPS data, and dispatch messages.

- Lock down third-party proof: video, witnesses, vehicle photos, and repair documentation.

It can also help to compare the claim to an ordinary auto crash investigation so you do not miss the basics. Our car accident page explains the standard evidence and insurance steps that still apply even when an app is involved.

Want the whole toolkit in a printable format for your file? Download the printable toolkit (PDF) and use it to track your documents and deadlines.

Louisiana Law Snapshot (Updated 2026)

Louisiana deadlines and fault rules can control whether a strong case stays strong. The key is to spot the right claim type early and treat the deadlines as evidence deadlines, not just court deadlines.

| Rule | Plain-English Meaning |

|---|---|

| Two-year delictual prescription | Louisiana Civil Code article 3493.1 generally provides a two-year time limit for many personal injury claims, so delays can risk losing the right to sue. |

| Comparative fault with a 51% bar after Jan. 1, 2026 | Louisiana Civil Code article 2323 uses comparative fault, and for causes of action arising on or after Jan. 1, 2026, recovery can be barred if you are found 51% or more at fault. |

Free Case Review: Protect the Evidence Before It Changes

We are not built for volume. We are built for leverage.

The Babcock Benefit mindset is simple: move fast on evidence, build a clean record, and stay trial-ready so pressure works in your favor. Call (225) 500-5000 and use the free case review form to get an evidence-first plan for your food delivery accident.

Call soon if video might overwrite, if the driver’s app status is disputed, or if insurers are pointing fingers about coverage. If you want to see the practice overview, read how we handle delivery-driver crashes and then bring your questions to the call.

These items are helpful to have with you when you call, but do not delay calling because you do not have them. If you have them handy, keep them nearby for the call.

- Photos of the scene and vehicle damage

- Names and contact info for witnesses

- The police report number or agency

- Screenshots of the order, app status, and any texts

- Insurance claim numbers and adjuster contact info

Call Today If Any of These Are True

- You are being asked to give a recorded statement right away

- Your car is about to be repaired or released from storage

- You think a platform policy or commercial policy should apply

- Fault is disputed and the other side is blaming you

- You need someone to send video preservation requests quickly

What Happens Next

- We triage the evidence: app records, photos, video sources, and insurance paperwork.

- We spot deadlines early and map who should be in the claim and why.

- We handle insurer contact strategy so pressure does not turn into a bad record.