Editorial & Legal Accuracy Notice (Louisiana)

This blog contains general legal and safety information and is not legal advice. Laws and deadlines can change, and outcomes depend on specific facts.

Last reviewed / updated: March 2, 2026

Reviewed, updated, and authored by: Stephen Babcock, Louisiana injury lawyer

This guide explains how towing and storage fees work after Louisiana wrecks, who typically pays, and how to protect your claim before the bill grows.

Towing and storage fees after a wreck can feel like a second collision. Your car gets hauled away, the yard starts charging daily storage, and the insurance claim moves at a different speed. If nobody pins down the facts early, the bill grows while everyone argues about who approved what.

Our approach is simple: turn a chaotic tow-yard situation into a clean, timestamped record. We are not built for volume. We are built for leverage. Speed + evidence preservation + insurer-insider knowledge + trial-ready preparation = The Babcock Benefit. For towing and storage fee disputes, leverage means stopping fee creep fast and proving every charge with documents.

Firm links: Client Reviews | Contact | Locations

Want a print-friendly version you can save and share? Download the printable toolkit (PDF) and keep it with your claim notes.

If you are inside the first 72 hours, call (225) 500-5000 or use the free case review form before evidence changes.

Who Pays Towing and Storage Fees in Louisiana After a Wreck?

In Louisiana, towing and storage fees after a wreck often get paid through auto insurance, but payment depends on coverage and what happened to the vehicle next. When the claim turns into a total-loss and title issue, Louisiana Revised Statutes §22:1292 is a key rule that addresses towing and storage charges.

| Situation | Who Often Pays | What You Should Save |

|---|---|---|

| You have towing/labor or collision coverage | Your insurer may pay, subject to limits and deductibles | Tow receipt, disabled-vehicle note, claim number email |

| Another driver is at fault | At-fault insurer may reimburse as property damage | Itemized invoice, photos, dates the insurer was notified |

| Police-ordered, non-consensual tow | Rates may be governed by PSC schedules depending on the tow | Tow slip, yard rate sheet, gate fee line items |

| Total loss + insurer assumes title steps | Payment duties can turn on title assumption and statutory rules | Written storage cut-off request, title/payoff emails, invoices |

If your immediate goal is getting the tow and storage invoice included in the vehicle claim, start with our Baton Rouge property damage claim page and focus on building a clean, chronological file. You can usually make progress faster by proving dates and documents than by debating fairness in a phone call.

LDI’s Consumer’s Guide to Auto Insurance notes that towing and labor coverage pays towing costs when your car is disabled and that many policies limit it to $25 per tow. That is why people get shocked when storage charges hit hundreds or thousands of dollars, because storage is a different line item that can keep accruing.

As a basic fault principle, Louisiana Civil Code art. 2315 is the starting point for why crash-caused expenses can be recoverable from the party who caused the harm. In real claims, though, you still have to prove the bill is tied to the wreck and tied to reasonable, documented dates.

How Do People Get Stuck With Tow-Yard Bills After a Crash?

People get stuck when nobody stops the fee meter and the yard keeps charging daily storage while the claim slows down. Louisiana Department of Insurance Directive 183 describes complaints about towing and storage charges on covered automobile losses and emphasizes compliance with Louisiana’s towing-and-storage rules.

- No one confirms the yard details: address, hours, daily rate, and release rules stay unclear.

- No written notice to the insurer: later, the carrier disputes when it learned where the car was.

- No itemized invoice: the bill has vague “fees” that are hard to challenge.

- No exit plan: the car sits while repair vs. total-loss decisions drag.

- Paperwork moves in circles: lien notices, title steps, and payoff letters delay release.

When Louisiana Revised Statutes §22:1292 applies, it restricts extra charges by stating that the daily storage fee is the only fee for storage services and it bars add-ons like locating the vehicle, photographs, and similar line items. If you are staring at a bill full of “administrative” extras, you need the itemization and the dates so you can compare what was charged to what is allowed in your situation.

Storage disputes also grow because people rely on verbal assurances that never get written down. This is why we push for a same-day email that lists the tow yard address, the daily rate, and the release requirements, because it locks the “known facts” before the story shifts.

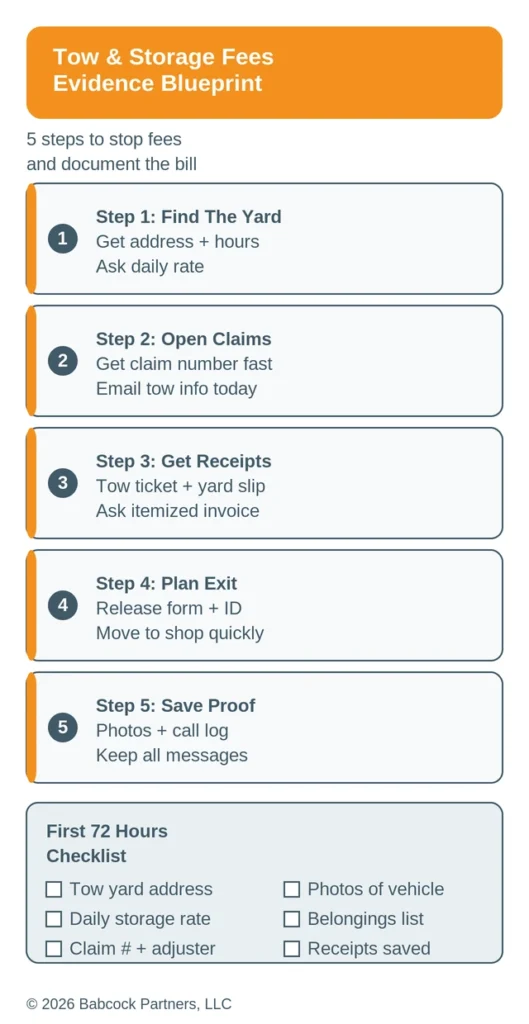

What Should You Do in the First 72 Hours After a Tow?

In the first 72 hours, focus on locating the vehicle, getting the daily storage rate in writing, and sending one clear notice email to the insurers involved. Those steps create a timeline that protects you if towing and storage fees after a wreck become disputed later.

- Confirm the tow yard address, phone, hours, and the daily storage rate.

- Ask what the yard needs to release the vehicle and who can authorize release.

- Open the claim and email the tow yard information to the adjuster the same day.

- Get the tow ticket, the storage agreement, and an itemized invoice.

- Photograph the vehicle and the lot tag or stock number at the yard.

- Remove personal property when allowed and list what you removed.

- Set an exit plan: repair shop, safer storage, or total-loss steps.

If you are dealing with gate fees or access to retrieve contents, Louisiana Revised Statutes §32:1734 addresses gate fees tied to stored vehicles and provides a framework for disputes about those charges. The practical move is still the same: get the yard’s rules in writing and keep the receipt trail clean.

How Do You Build a Tow-and-Storage Timeline Insurers Can’t Ignore?

A tow-and-storage timeline is a one-page record that shows where the car was, what the yard charged, and what you asked the insurer to do about it. When you attach the invoice and the notice email, you shift the discussion from opinions to dates and documents.

| Time Marker | What to Write Down | Proof to Save |

|---|---|---|

| Day of crash | Who towed it, why it was towed, and where it went | tow slip, photos, witness names, dispatch info |

| First contact with yard | Daily rate, gate fees, release requirements, hours | rate sheet, written confirmation, recorded name/time |

| First contact with insurer | Claim number, adjuster, date you provided location | email notice, screenshots of upload portals, call log |

| Decision point | Repair vs. total loss, shop transfer plan, storage cut-off request | repair estimate, adjuster emails, written approvals |

| Release/transfer day | Who picked it up, where it went, final invoice total | final invoice, receipt, mileage/condition photos |

LDI’s Guide to Auto Insurance After an Accident explains the basics of the claims process and why organized documentation matters when disputes arise. Your goal is not a perfect story; your goal is a verifiable story that is hard to contradict.

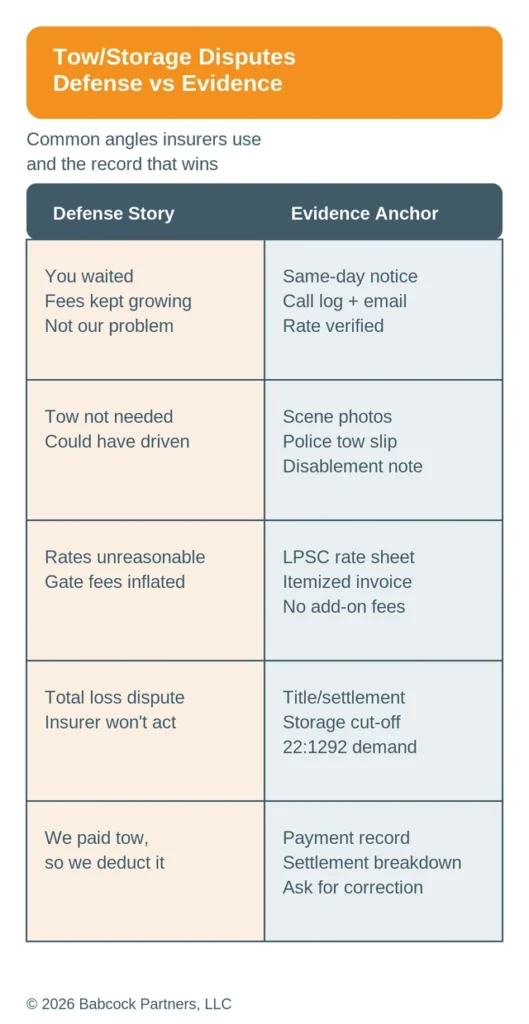

What Arguments Do Insurers Use to Deny Tow and Storage Charges?

Insurers often dispute tow and storage charges by calling them unnecessary, unreasonable, or avoidable. The fastest way to respond is a clean record: an itemized invoice, photos, and a notice email that anchors the dates.

| Defense Angle | Evidence That Answers It |

|---|---|

| “You waited, so storage is on you.” |

|

| “Tow wasn’t needed.” |

|

| “The rate is unreasonable.” |

|

| “Those add-on fees are not covered.” |

|

| “We paid tow, so we deduct it.” |

|

For non-consensual towing situations, the Louisiana Public Service Commission’s towing and recovery order includes a rate schedule and invoice rules that can help anchor what “reasonable” looks like for that category of tow. If the tow was consensual, you still want the same thing: the yard’s written rate and a clean invoice.

When Louisiana Revised Statutes §22:1292 applies, it limits storage charges to a daily fee and bars add-on “service” charges for common tasks like locating or photographing the vehicle. That is what we mean by leverage when we demand an itemized invoice and challenge extra line items early, because it can reduce the bill before it becomes the headline issue in the claim.

What Happens to Tow and Storage Fees When the Vehicle Is Totaled?

When a vehicle is totaled, towing and storage fees after a wreck can rise while the claim shifts into title and payoff paperwork. Louisiana Revised Statutes §22:1292 matters in that scenario because it ties towing and storage obligations to when an insurer assumes title on a covered loss.

- Ask “repair or total?” in writing: get the decision path and the next step from the adjuster.

- Request a storage cut-off date: ask the carrier to confirm when storage stops accruing.

- Ask who pays the yard directly: confirm whether payment goes to you or to the storage facility.

- Demand a line-item settlement: insist on a breakdown if the carrier claims it “already paid” towing.

Louisiana Revised Statutes §32:702 includes a definition of “total loss” tied to repair costs relative to actual cash value, and that definition often drives when the claim changes gears. If you need help fitting towing and storage into the larger valuation and settlement picture, our property-damage claim help page explains common friction points that show up in total-loss files.

If the tow was non-consensual, Louisiana Revised Statutes §32:1728 includes limits on charging storage beyond certain time periods and requires notices in that context. You do not need to memorize the law to protect yourself, but you do need dates, invoices, and written notice to the insurer.

What we see in practice

We rarely see tow disputes that turn on one dramatic invoice line. We usually see small delays, missing emails, and unclear release rules that let storage fees stack up.

- We see storage bills grow because nobody confirms the daily rate and yard rules on Day 1.

- We see adjusters push back hardest when the invoice is not itemized or the dates do not line up.

- We see people pay out of pocket under pressure, then struggle to get reimbursed without a clean paper trail.

- We see “offset” confusion when a carrier pays a vendor but reduces the settlement without explaining the math.

- We see faster resolutions when the owner sends one short, documented timeline instead of ten phone calls.

How Do You Keep a Tow and Storage Dispute From Derailing Your Claim?

You keep the dispute small by turning it into a short, documented timeline with receipts and written notice. Then you make the adjuster respond to specifics instead of debating the bill in general terms.

- Send one packet: invoice, tow receipt, photos, and your timeline on one email thread.

- Ask one clear question: “Which dates or charges are you disputing, and why?”

- Push for a written storage cut-off: get confirmation of the stop date.

- Track all payments: ask whether the carrier paid the yard directly and request proof.

- Keep your own duplicates: save PDFs, photos, and email headers in one folder.

Louisiana Revised Statutes §22:1892 contains insurer claim-handling duties and timelines that are triggered by satisfactory proof of loss, which is one reason a clean documentation packet matters. This is why we focus on building proof first and arguing later, because a vague claim file gives the insurer room to delay and dispute.

Talk to a Lawyer Quickly If…

Talk to a lawyer quickly if the bill is growing daily and nobody will confirm a storage cut-off date in writing. You should also move fast if the insurer is pushing you to sign documents you do not understand just to get the car released.

- The tow yard refuses to release the vehicle without payments you cannot verify.

- The insurer says “we won’t pay storage” but will not explain which charges it disputes.

- You are being pressured to accept a quick settlement while documents are missing.

- The vehicle is totaled and title/payoff steps are stalling release.

For a print-friendly checklist you can share with family members who are helping with the claim, Download the printable toolkit (PDF) and keep it with the tow yard paperwork. That way everyone uses the same timeline and the same document set.

Louisiana Law Snapshot (Updated 2026)

Louisiana has a two-year delictual prescription period for many personal injury and related civil claims, and La. Civ. Code art. 3493.1 is the key starting point for the deadline discussion. Louisiana also uses comparative fault, and La. Civ. Code art. 2323 reflects the post–Jan. 1, 2026 rule that bars recovery when a claimant is 51% or more at fault.

| Rule | Plain-English Meaning | Why It Matters for Tow/Storage Disputes |

|---|---|---|

| Two-year prescription | There is a time limit to file most lawsuits, and waiting can cost you rights. | A growing tow bill is not a reason to “wait and see,” because deadlines can run while you try to negotiate. |

| Comparative fault + 51% bar | Fault can reduce recovery, and majority fault can bar recovery under the updated rule. | Accident facts still matter in property and fee disputes, so preserve the crash evidence early. |

This information is general and does not replace legal advice about your specific deadlines. If you are unsure which rules apply, get a lawyer to review the facts promptly.

Free Case Review: Stop Fee Creep and Protect the Claim

We are not built for volume. We are built for leverage. If towing and storage fees after a wreck are escalating, leverage often comes from fast notice, clean documentation, and a clear plan to stop storage from accruing.

If you want a bigger picture on vehicle claims, start with our vehicle property damage case page, then call (225) 500-5000 and use the free case review form to get your timeline reviewed. We will explain the next evidence steps in plain English and keep the focus on proof, not pressure.

These items are helpful to have with you when you call, but do not delay calling because you do not have them. If you have them handy, keep them nearby for the call.

- Tow yard name, address, and daily storage rate

- Tow receipt and the most recent itemized invoice

- Claim numbers and adjuster contact information

- Photos of the vehicle and any lot tag/stock number

- Any emails or texts about release authorization

Call Today If…

- The tow yard says the bill is increasing daily and you cannot get answers

- The insurer refuses to confirm a storage cut-off date in writing

- You are being pushed to accept a quick settlement while paperwork is missing

- The vehicle is totaled and title/payoff steps are stalling release

What Happens Next

- We triage evidence and build a clean timeline from invoices, photos, and notices

- We spot deadlines and pressure points so the claim does not drift

- We help set an insurer contact strategy aimed at documenting disputes and forcing clarity